The Federal Reserve cut rates by 25 basis points, lowering the target range to 4.0–4.25%.

Powell said it was ‘another step toward a more neutral policy stance’ and that policy was ‘not on a preset course’ — framing the move as a temporary adjustment to shifting conditions rather than the start of a full pivot.

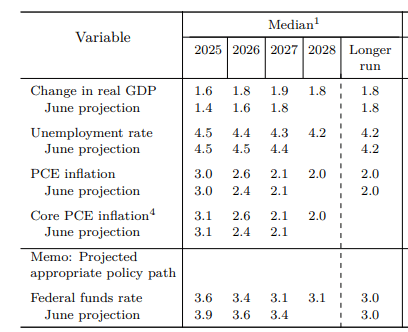

But the move came with inflation running above target for more than four years straight — the longest stretch since the late 1990s. And according to the Fed’s own September 2025 projections, PCE inflation is expected to remain above 2% until 2028, while the federal funds rate is forecast to decline from 3.6% in 2025 to 3.1% in 2027. Normally, higher rates are used to tame persistent inflation, but the Fed is charting a path of loosening policy instead.

From hawkish pledges to capitulation

Only weeks earlier at Jackson Hole, Powell wrapped himself in hawkish feathers, pledging: “Come what may, we will not allow a one-time increase in the price level to become an ongoing inflation problem.”

That was supposed to be a red line, yet Powell has erased it himself with this cut. He called it risk management, but in reality, it looks more like surrender. Of course, Powell defended the move, but the markets interpreted it as dovish, and risk assets surged.

Excess liquidity masks real risk

The credit market makes the absurdity blindingly obvious — junk debt trades like blue chips, as if risk had vanished. The U.S. high-yield spread — the extra yield investors demand to hold risky corporate debt instead of safe Treasuries — has collapsed to just 2.9%, near cycle lows, while CCC-rated junk debt, the r

Go to Source to See Full Article

Author: Mike Ermolaev