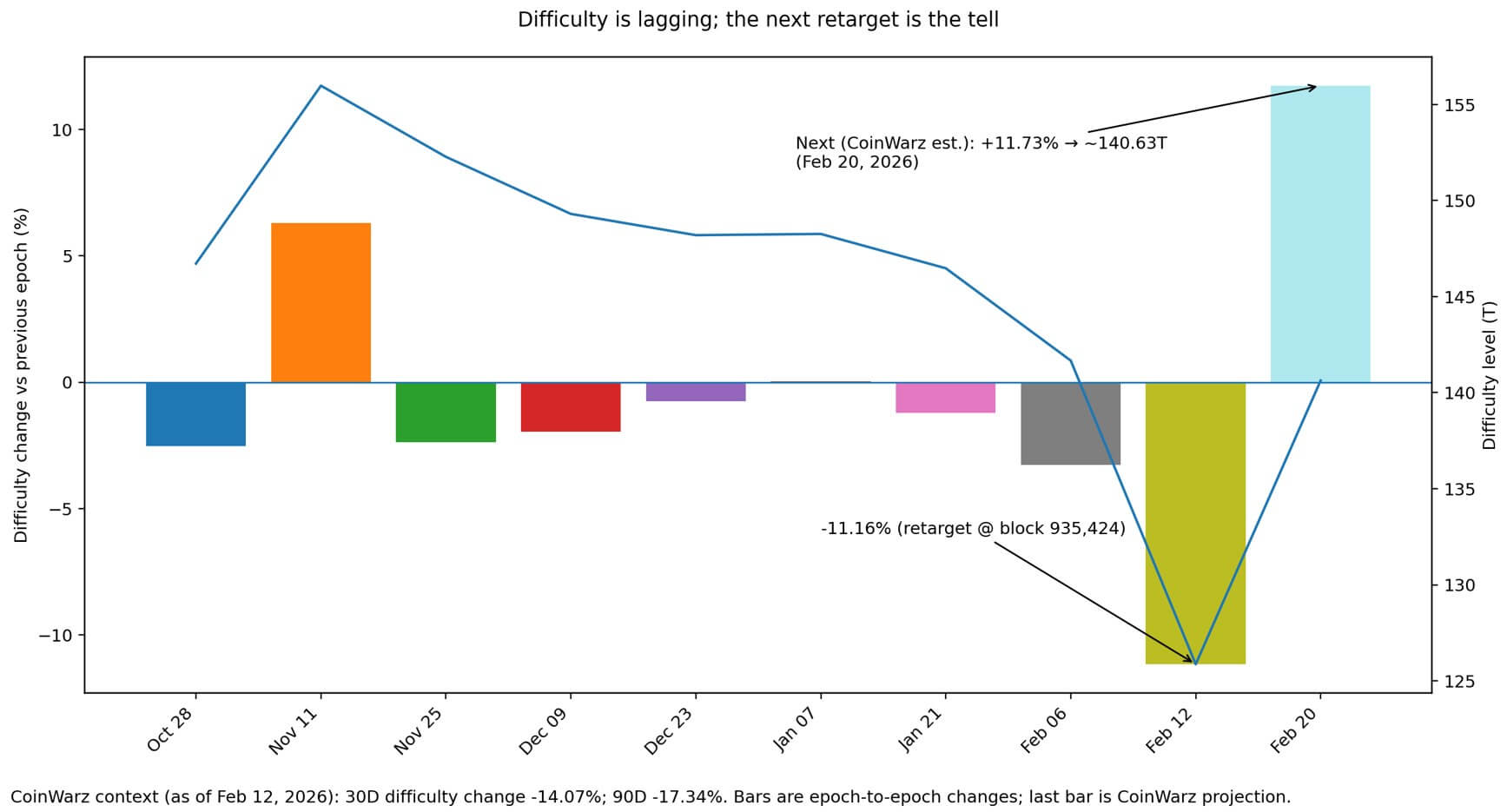

Bitcoin’s mining difficulty decreased by 11.16% to approximately 125.86 trillion at the most recent retarget boundary around block 935,424.

That marks the largest negative adjustment since the 2021 China mining ban, the sixth consecutive downward retarget, and the tenth largest negative adjustment in Bitcoin’s history.

However, difficulty adjustments are lagging indicators, as they reflect what occurred over the previous 2,016 blocks rather than what’s happening now.

The real question is whether the machines that went dark are coming back, or whether this retarget marks the start of a deeper miner shakeout.

The most useful forward signal is the next adjustment. CoinWarz is already estimating a 12% rebound around Feb. 20, which implies that hashrate is returning fast.

This is a movement more consistent with curtailment and short-term economics than with a structural miner exodus. If that rebound fails to materialize and the difficulty continues to decline, then “capitulation” becomes more than a headline.

Three drivers, only one tied to capitulation

The difficulty drop indicates slower block times relative to the previous epoch, indicating that less hashrate was online.

Yet, three distinct forces can push hashrate offline, and they don’t all mean the same thing.

Forced curtailment and outages are transitory. Winter Storm Fern hammered US miners in early February, forcing grid-connected operations to shut down during peak demand.

Foundry’s pool hash reportedly dropped roughly 60% during peak disruption. When miners curtail operations during grid emergencies, the hashrate disappears overnight and can return just as quickly once the weather clears.

That kind of offline event looks dramatic in difficulty numbers, but doesn’t signal financial distress.

Economics-driven shutdowns are capitulation-adjacent.

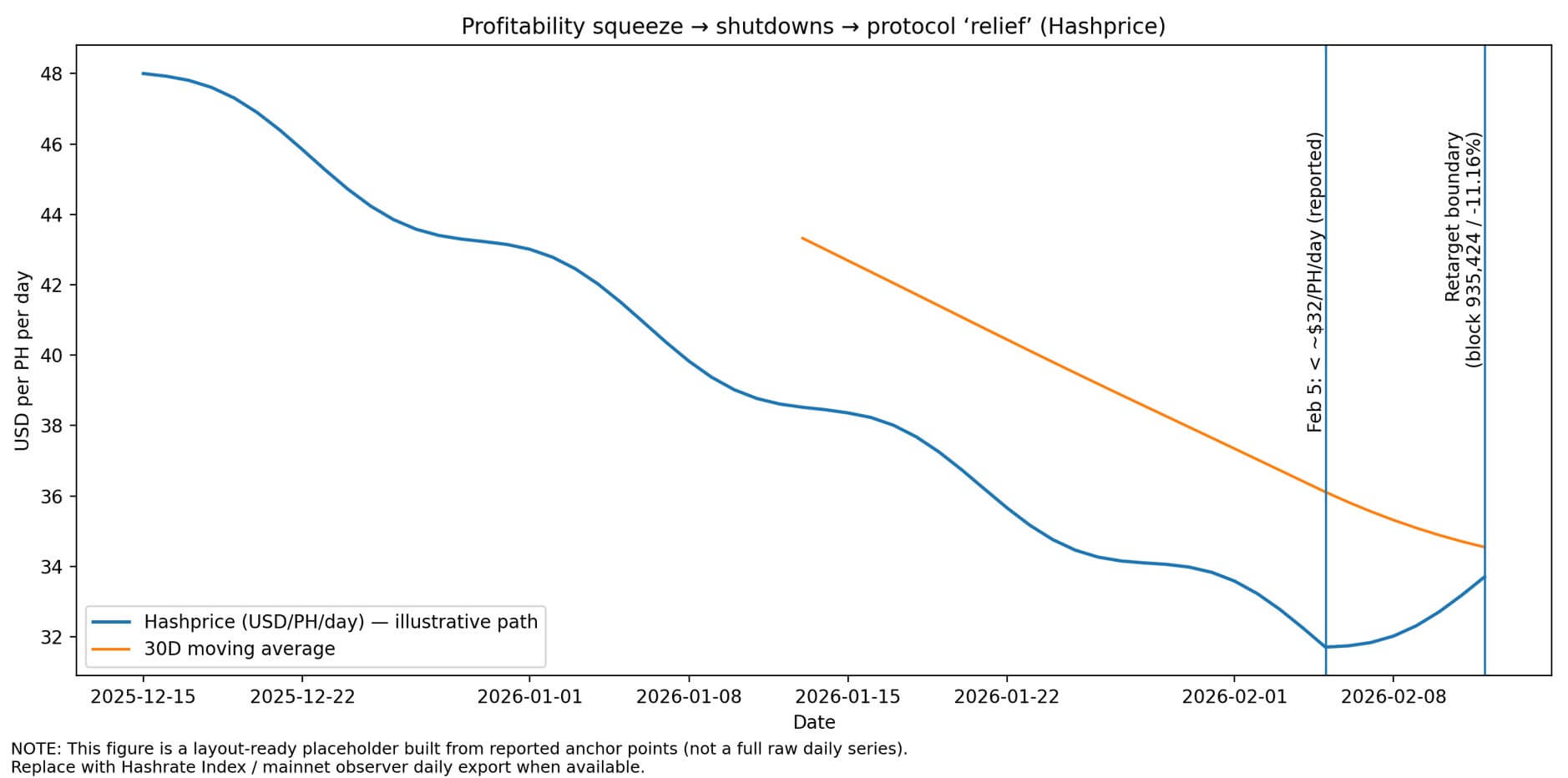

The revenue per unit of hashrate, called hashprice, printed record lows in early February. TheEnergyMag reported hashprice falling below $32 per petahash per day, and Hashrate Index data shows live hashprice hovering in the low $30s.

When hashprice is crushed, marginal fleets running older ASICs or paying higher power costs shut off. That can be capitulation, but it can also be rational idling: miners waiting for difficulty to reset and profitability to improve before turning machines back on.

The protocol rewards that patience. Cutting difficulty 11.16% raises expected Bitcoin earned per unit hash by roughly 12.6% until the hashrate returns, creating a short profitability honeymoon for survivors.

Structural shifts represent slow-burning capitulation. Some miners are increasingly treating Bitcoin mining as an optional workload, with AI and high-performance computing data center pivots appearing alongside stress coverage for miners.

If firms are reallocating capital from ASICs to data centers, the hashrate that goes offline may not return, at least not quickly. That’s a different kind of capitulation: a strategic exit.

Capitulation checklist: what to watch

A double-digit negative retarget can mean very different things depending on subsequent events. Treat it like a diagnostic test rather than a verdict.

Protocol and hashrate behavior indicate whether machines are returning. Hashrate rebound speed is the clearest signal: a rapid snapback within hours or days indicates curtailment, while a slow grind suggests deeper stress.

The next retarget projection is your proxy. CoinWarz’s 12% rebound estimate implies the hash is already returning. If that projection holds, the difficulty drop was a lagging artifact of temporary offline capacity.

Difficulty path over multiple epochs matters, too. A single large cut followed by a rebound isn’t capitulation; multiple consecutive cuts define a stress regime.

The last 30 to 90 days have already seen cumulative difficulty decline in the double digits, which means this retarget wasn’t the first sign of trouble, just the loudest.

Changes in pool concentration can reveal the reallocation of real-world capacity. If big pools lose market share structurally rather than temporarily, that’s a signal that mining infrastructure is changing hands or going offline permanently.

Foundry’s disruption during the storm is worth watching in that context.

Miner economics explain why machines shut off in the first place. Hashprice versus “pain thresholds” is the core metric.

Record or near-record lows are when marginal rigs go dark. A Bitcoin price drawdown relative to difficulty creates a squeeze: if price falls faster than difficulty can reset, stress spikes.

That’s the macro tie-in for why this happened now. Fee support, the share of block rewards coming from transaction fees rather than the subsidy, also matters.

If fees aren’t cushioning the subsidy, miners live or die on price and efficiency. Low fee environments amplify hashprice stress.

Balance-sheet stress is where true capitulation usually shows up.

Miner selling pressure, consisting of spikes in miner-to-exchange flows or reserve drawdowns, signals forced liquidation.

Public miner financing behavior, like emergency debt or equity raises, asset sales, or restructuring language, also flags distress.

ASIC secondary-market pricing is another tell: sharp drops in used ASIC prices suggest forced liquidation, while stable pricing suggests temporary offline capacity instead of bankruptcy.

Weather, economics, or structure

Weather whiplash is the transitory case. Curtailment and outages push hashrate offline, difficulty drops, and hashrate returns quickly once conditions normalize.

In this scenario, the next retarget would flip positive, exactly what CoinWarz is projecting. This scenario means the difficulty drop was mostly operational.

The network adjusts, profitability improves for those who stayed online, and offline capacity returns.

Economic shakeout is classic capitulation. Hashprice stays depressed, Bitcoin price remains weak, and older fleets stay offline because running at a loss makes no sense.

You’d see repeated negative adjustments over multiple epochs, elevated miner selling, and falling ASIC resale prices.

That creates short-term sell pressure risk and longer-term industry consolidation as weaker operators exit and stronger ones acquire distressed assets.

Structural reset is the path to reallocating data centers. Some firms treat mining as interruptible and reallocate capital to AI or high-performance computing. Hashrate becomes more seasonal and price-sensitive, leading to choppier difficulty adjustments and larger swings.

Bitcoin’s security budget is increasingly tied to broader compute and energy markets. That’s not a crisis, but it does change the dynamics of how hashrate responds to price.

| Signal | If curtailment / outage | If economics capitulation | If structural exit | Where to pull the data |

|---|---|---|---|---|

| Next retarget direction & size | Fast rebound (next epoch flips positive) as curtailed hash comes back quickly | Weak/flat rebound or more negative retargets if marginal fleets stay offline | Choppy / repeated down epochs even after the “relief” because hash doesn’t return | CoinWarz “Bitcoin Difficulty Chart” (next estimate + blocks remaining). (coinwarz.com) |

| Avg block time (current epoch) | Block times snap back toward ~10 min within days as hash returns | Block times stay slow (>10 min) because shutdowns persist until profitability improves | Block times remain volatile (hash becomes more interruptible/seasonal) | CoinWarz difficulty chart + hashrate chart includes current block time. (coinwarz.com) |

| Hashprice ($/PH/day) + 30D MA | Hashprice stabilizes/rebounds after the event; shutdowns were operational | Hashprice stays near pain thresholds (e.g., “< ~$32/PH/day” reports) → marginal rigs off | Hashprice recovers but capex still shifts away from ASIC growth; mining becomes “optional” | Hashrate Index live “Hashprice $/PH/DAY” + definition page; record-low coverage (TheMinerMag/TheEnergyMag). (hashrateindex.com) |

| Fee support (fees % of total reward) | Fees can mask downtime; no sustained stress if fee share is elevated | Low fee share + low price = worst squeeze; stress amplified | Persistent low fees make mining more dependent on power efficiency + alternative revenue models | Bitbo “Fees as % of Total Block Reward”. (Bitbo Charts) |

| Pool share dislocations (e.g., Foundry disruption) | A large pool’s share drops then normalizes (temporary curtailment) | Smaller/high-cost pools lose share; consolidation toward efficient operators | Durable geographic/pool share reshuffle as infra changes hands or exits | Hashrate Index pool distribution + Cointelegraph/TradingView report on Foundry’s storm-driven drop. (hashrateindex.com) |

| Miner selling pressure (confirming signal) | No major sustained spike in miner→exchange flows; reserves broadly stable | Spikes in miner→exchange flows + miner reserves down (forced liquidity) | Sustained net outflows / declining miner balances over weeks-months (strategic distribution) | CryptoQuant “Miner to Exchange Flow (Total)” + “Miner Reserve”; Glassnode “Miner Balance”. (Cryptoquant) |

| ASIC resale prices (liquidation vs orderly idling) | Prices broadly stable; used market doesn’t gap down | Used ASIC prices drop sharply (esp. older tiers) → liquidation | Prolonged softness in ASIC pricing (capex redirected), slow recovery in demand | Hashrate Index ASIC Price Index. (data.hashrateindex.com) |

What the rebound tells

The next retarget is the cleanest test of which scenario is playing out. If hashrate snaps back and difficulty rebounds as CoinWarz projects, the “capitulation” narrative fades.

The drop was real, but it reflected temporary disruptions, such as weather, short-term economics, and rational idling.

Miners who stayed online captured the profitability honeymoon, the difficulty resets to match the returning hashrate, and the network moved on.

The stress only gets deeper if the rebound doesn’t materialize, which is unlikely. Yet if difficulty declines for two to three more epochs, that would imply the offline hashrate isn’t coming back quickly, either because the economics don’t support it or because the capital has moved elsewhere.

In that case, the expectation is that the balance sheet stress signals will start flashing: elevated selling, financing scrambles, and ASIC liquidation.

The difficulty drop itself is backward-looking.

It confirms that a meaningful share of hashpower was offline over the last two weeks, some for economic reasons and some for operational reasons.

What matters now is whether those machines are coming back, and the answer will show up in the data over the next week.

The protocol doesn’t care about narratives, it just adjusts to whatever hashrate shows up.

Whether this retarget was a transitory blip or the start of a miner exodus depends on what happens next, not what already happened.

Go to Source to See Full Article

Author: Gino Matos